An Optimal Approach to Your

Investment Relationship

Markets change. Headlines come and go. Sound principles endure.

Begin with Frederick Ravid’s latest perspectives on investing, economics, and today’s financial landscape.

Then explore the philosophy and services that define the MoneyGrow® approach.

Insights from Frederick Ravid

Articles and commentary designed to help you navigate financial choices with greater confidence and clarity.

My Visit to the New York Stock Exchange

The Semiconductor Sell-Off: Have the Business Fundamentals Changed?

Shamrock Syndrome

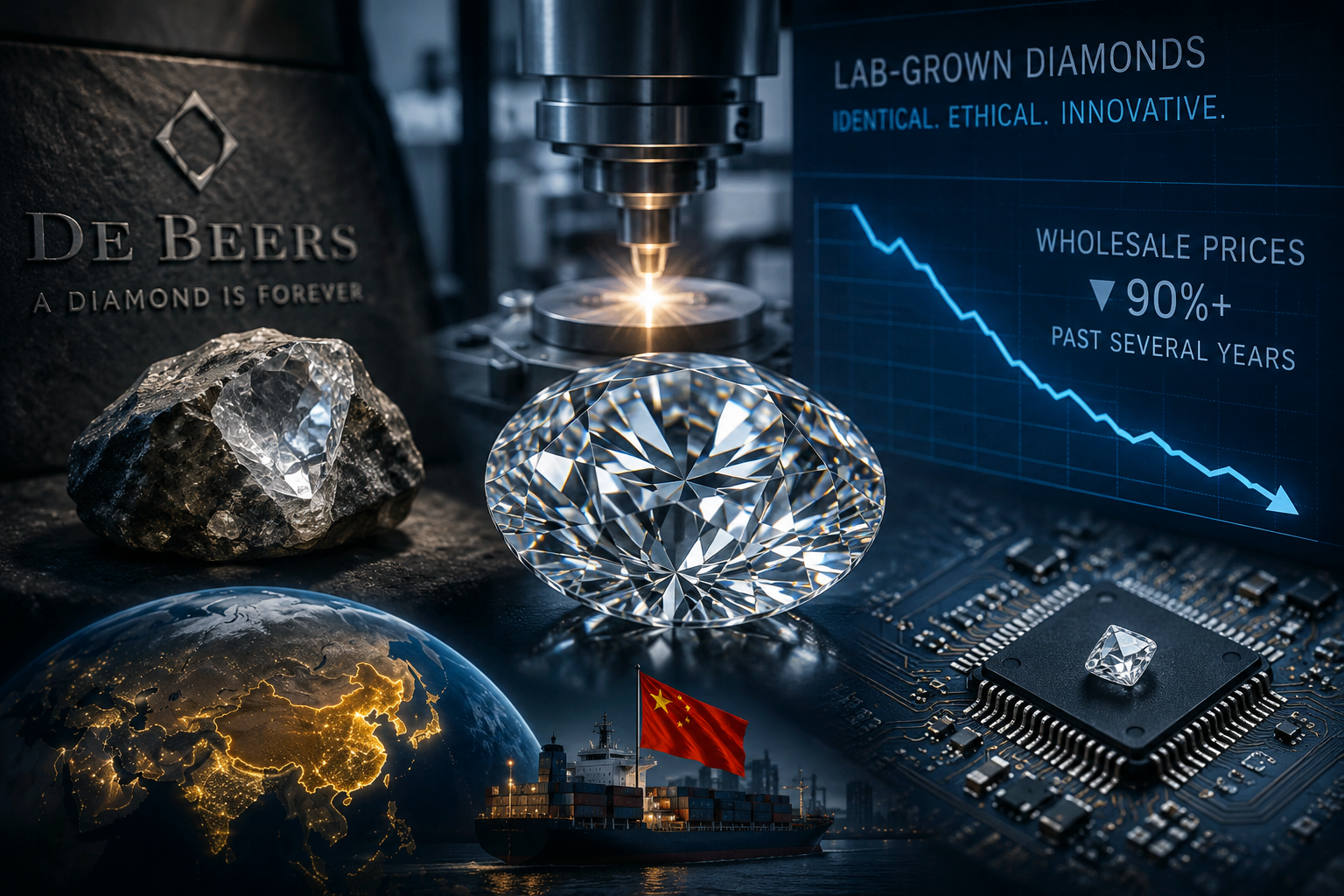

Diamond Industry Secrets That May Surprise You

The Meltdown of Meta Platforms

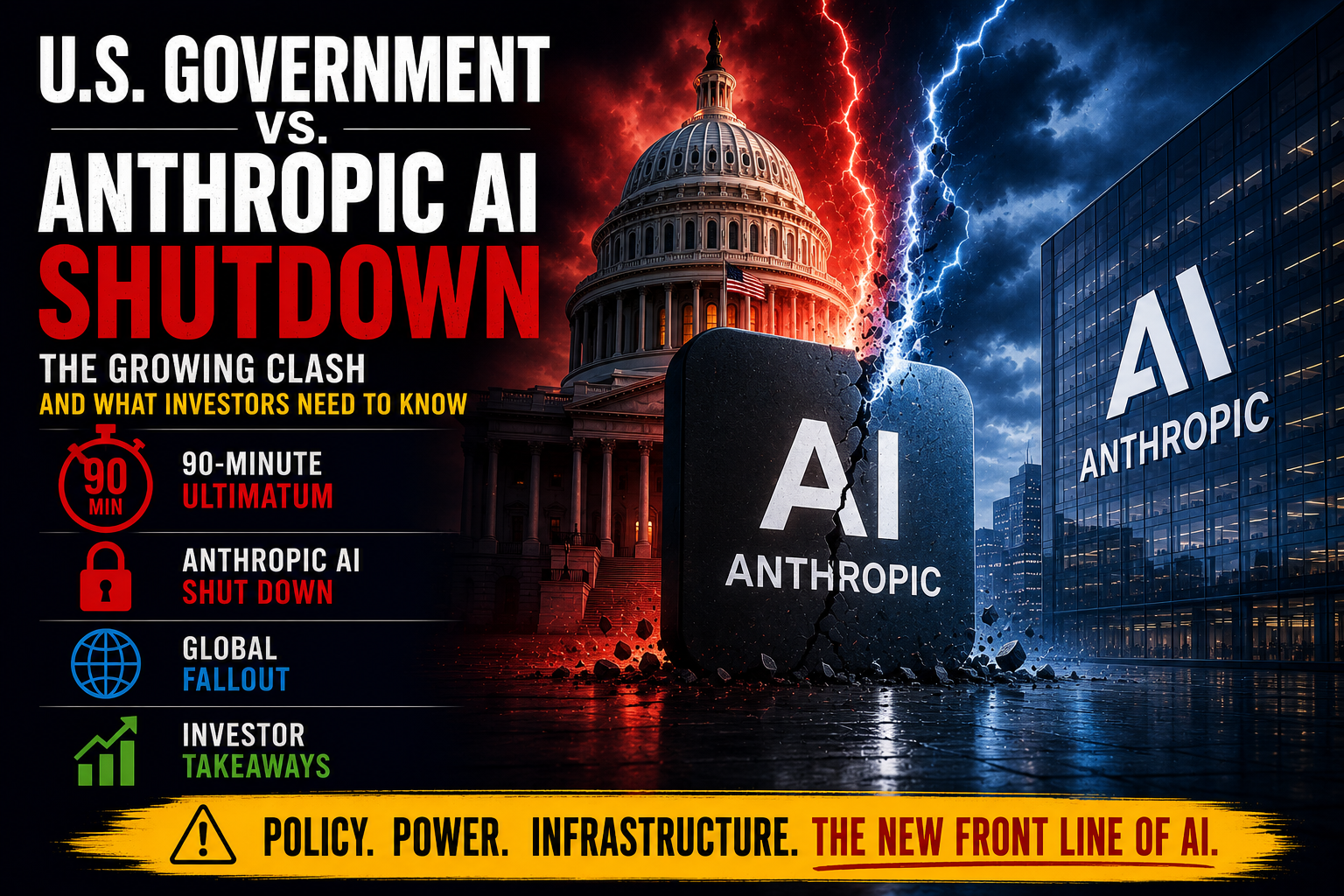

Shocking U.S. Government vs. Anthropic AI Shutdown and How Investors Are Affected

A Unique Investor Partnership built on Experience, Clarity, and Concierge Level Service

- Discover how Moneygrow® can enhance control through personalized financial planning and investment management.

- Explore timely insights and practical perspectives to help you make more informed financial decisions.

- Understand the principles that guide every recommendation and learn why a fiduciary relationship matters.

- See how technology keeps your financial life organized with secure, 24/7 access to your complete financial picture.

- Learn what sets Moneygrow® apart and why clients choose a relationship built on trust, transparency, and personal attention.

A Perspective Shaped by Experience

After over 9,600 trading days in the asset management field, I have seen countless investment strategies come and go. Many appeared compelling at first, but over time I learned where they fell short and what truly creates lasting value.

As my experience deepened, so did my understanding of the industry itself. Too often, the investment industry produces generic, unremarkable results while failing to sensitively produce portfolios that actually make sense in this dynamic economic environment. You deserve better.

I believe the vast majority of investment relationships follow an obsolete model. Sales pressure, lack of consistent personal attention and obligation to clients, and conflicts of interest are epidemic. We choose to be different because it’s the right way to provide long-term attentive service. This is what YOU need.

What you don’t need is to be turned into a number immediately upon getting into a relationship that proves to be generic. Your specific needs, values, and challengs need to be addressed and remain in the forefront of the relationship at all times.

–Frederick Ravid, ChFC®

Ways we help you Enhance Financial Control

Helping you navigate every stage of your financial life with independent, fiduciary guidance tailored to your goals.

A Responsible Approach to the Future

The MoneyGrow® principles of Invest in Life begin with you. We believe exceptional personal service, thoughtful guidance and consistent attention are the foundation for making better financial choices and peace of mind.

- Genuine client service over the long term is rooted in fiduciary guidance rather than the sale of financial products or sales commissions.

- Investment should serve more than the pursuit of profit. It should contribute to a stable, resilient, and balanced world.

- We all share a responsibility to consider the long-term consequences of our financial choices.

- Looking beyond short-term gains encourages stronger businesses, healthier markets, and more durable wealth.

- When investment reflects stewardship, resilience, and fairness, it can help shape a better future.

A better future is possible, and thoughtful financial choices can help shape it.

An Active Advisory Relationship Makes All the Difference

Many advisory relationships become less active over time. We believe thoughtful fiduciary guidance should remain consistent as your financial life evolves.

Our role is to help you avoid two of the greatest long-term financial risks:

- Information overload from financial media, AI-generated content, marketing, and conflicting opinions.

- Procrastination caused by uncertainty or feeling overwhelmed.

Regular reviews and the award-winning Moneygrow® Client Portal help keep you informed, engaged, and aligned with your long-term goals.

The Moneygrow® Technical Advantage:

You deserve complete, effortless access to the information that supports your financial life. The Moneygrow® Client Portal is built on robust, modern technology that keeps every detail clear, organized, and up to date with just a click.

Behind the scenes, our advanced internal systems support thoughtful investment selection, diligent oversight, and responsive account management. Your trading and account resources are maintained with industry-leading security and quality standards, ensuring that your financial information is protected and your experience is seamless.

Our goal is simple: to give you the clarity, confidence, and transparency you need to stay fully informed and fully in control.

Beyond the Pursuit of Profit

Investing with Purpose

Profit alone is not enough. Your financial choices should reflect your values, your long-term goals, and the legacy you hope to leave.

Moneygrow® provides active fiduciary guidance built on consistent attention, thoughtful stewardship, and an investment philosophy that looks beyond short-term market results.

Many advisory relationships become less engaged over time. We believe the greatest value we provide is remaining actively involved as your financial life evolves.

This is what it means to Invest in Life.

Our Commitment

We are here to restore a sense of justice and accountability to the way your money is put to work. Your investments should strengthen your life, your values, and the world you want to see.

Not yet a client?

Discover how Moneygrow® can help you build a more confident financial future. Schedule a complimentary consultation and learn how your secure Client Portal gives you convenient access to your financial information, planning tools, and ongoing guidance.